Mohammad Ali Ghanamizadeh Fallahi

Introduction

The foreign policies of nations undergo profound transformations in response to global shifts. States lacking the requisite adaptability are sidelined from the geopolitical arena and either occupy no position or are relegated to the lower tiers of the global power hierarchy. Conversely, even countries pursuing multifaceted and flexible foreign policies do not invariably achieve their objectives and may fail to secure a prominent place in the power hierarchy, thereby consigning themselves to an unfavorable destiny. Numerous factors influence the evolution of decision-making mechanisms, diplomacy, and foreign policy in states. Geo-economics, geopolitics, prevailing ideology, and related phenomena all exert a significant impact on foreign policy formulation and a country’s international standing. Nevertheless, geopolitics continues to play an exceptionally pivotal role among these determinants.

Türkiye exemplifies this dynamic through its strategically valuable geography. Positioned at the crossroads and choke-points of global trade and transit routes, and exercising control over critical maritime passages such as those linking the Black Sea to the Mediterranean, Türkiye occupies a distinctive position among great powers. Yet this geographical endowment has consistently functioned as a double-edged sword. Although Türkiye possesses highly significant geopolitical leverage, it is entirely devoid of indigenous oil and natural gas reserves. Moreover, the very possession of such strategic geography invites persistent intervention by major superpowers. The lingering trauma of the Ottoman Empire’s collapse, the Sèvres Syndrome, and the enduring Kurdish question have all profoundly shaped the DNA of Turkish foreign policy, rendering it inherently multidimensional. As Ibrahim Kalın has aptly observed, Türkiye enjoys a “precious loneliness”; should it abandon this autonomy and fully integrate into either the Eastern or Western bloc, it would forfeit its strategic independence. It was within this context that Ahmet Davutoğlu’s doctrine of strategic depth and the concept of strategic autonomy were forged within Türkiye’s foreign policy apparatus.

Despite its commanding geopolitical position, Türkiye suffers from one critical vulnerability: the complete absence of domestic oil and natural gas deposits. Consequently, it remains heavily dependent on imports of natural gas from Russia, Iran, and Turkmenistan. However, with the emergence of the “battle of corridors” and China’s Belt and Road Initiative, Türkiye without possessing a single barrel of oil or cubic meter of natural gas has transformed itself into a regional energy hub. Today, it boasts one of the world’s most modern fleets of liquefied natural gas (LNG) carriers and floating storage and regasification units, ranks fifth in clean energy production capacity within Europe and eleventh globally, and has recorded remarkable growth in solar panel manufacturing.

In the evolving international order, novel variables are emerging that fundamentally alter the rules of the game and the decision-making calculus of states’ foreign policies. Rare-earth elements (REEs) constitute one such transformative factor. Advanced military and defense industry particularly the airframes of missiles and fighter aircraft semiconductor chips essential for artificial intelligence, high-technology electronic components, high-performance permanent magnets used in electric vehicles, wind turbines, and consumer electronics, mobile telephones, hard-disk drives, petroleum-refining catalysts, catalytic converters, phosphors in LED displays, televisions, lasers, advanced batteries, and modern defense systems all depend critically on REEs owing to their unique magnetic, optical, and chemical properties.

A new domain of great-power competition has thus materialized, in which control over the discovery, extraction, and processing of these elements has assumed paramount strategic importance. This has given rise to concepts such as the “underground war,” the “battle of the mines,” and, more recently, the “battle for rare-earth supply-chain dominance.” In an era when numerous states are striving for primacy in emerging competitive domains, Türkiye has not remained on the sidelines. It is actively cultivating new instruments of statecraft to optimize its agency amid great-power rivalry: achieving approximately 80 percent self-sufficiency in defense industries, establishing itself as the principal gas hub for the Caucasus and Central Asia, conducting ship-to-ship LNG transfers through Iraqi ports and deliveries to Egypt via floating storage units, and registering dramatic advances in renewable energy. These developments collectively signal Türkiye’s deliberate pivot toward soft-power projection and its entry into a strategic arena where hard military power alone no longer yields decisive outcomes.

Türkiye Rises to Join the Global Rare Earth Elements Supply Chain

One of the most consequential developments that has reshaped Türkiye’s strategic positioning, as well as its roles in the Caucasus, Central Asia, and Anatolia yet received scant international attention was the discovery of vast rare-earth element (REE) deposits within the country. Fatih Dönmez, then Minister of Energy and Natural Resources, announced that Türkiye had identified the world’s second-largest reserve of rare-earth elements in the Beylikova district of Eskişehir Province, located in central Anatolia. This field is estimated to contain 694 million metric tons of ore, placing it behind only China’s Bayan Obo deposit, which holds approximately 800 million metric tons. Dönmez emphasized that the deposit’s proximity to the surface would render extraction comparatively cost-effective. He further noted, “Of the 17 recognized rare-earth elements, we will be able to produce 10 from this site. Moreover, the new reserve will enable the annual processing of approximately 570,000 metric tons of ore.” He also revealed that the site could yield 250 metric tons of thorium annually, an element with applications as a nuclear fuel.

Among the most significant elements identified in this deposit are lanthanum, cerium, and neodymium—critical materials extensively utilized in automotive manufacturing, particularly for permanent magnets in electric vehicles (EVs), wind turbines, and defense industries. Over the past several years, Türkiye has achieved substantial growth in EV production and sales. This trajectory has allowed the country to leverage its established soft-power assets by integrating clean and renewable energy imperatives into its market strategies, thereby enhancing its global influence through EV exports, especially to European markets. Should the exploitation of these REE deposits be accelerated through judicious and timely measures, Türkiye could secure a more prominent position in the supply chains for automotive production, EV batteries, and renewable energy technologies. Consequently, the geo-economic significance of Türkiye would eclipse its geopolitical dimensions hitherto centered on security concerns positioning the country as an exemplary economic model for European and Middle Eastern markets.

Thus, should the reported scale of Türkiye’s REE discoveries prove accurate and advance to industrial exploitation, the nation could emerge as a pivotal actor in the global REE landscape, playing a substantive role in supply chains for clean-energy equipment and defense industries; this prospect is particularly salient given China’s current dominance, controlling over 80 percent of production and a substantial share of processing. In the automotive sector, the best-selling model in the market was the domestically produced Togg T10X, Türkiye’s inaugural electric vehicle, which recorded 30,094 units sold. Ranking second was the Tesla Model Y with 11,534 units, while the BYD Atto 3, with 2,252 units, secured eighth place. The expansion of electric mobility in Türkiye has been vigorously supported through fiscal incentives, notably under special consumption tax regulations that incentivize both domestic production and imports of EVs. As a result, multiple manufacturers have imported models qualifying for the reduced 10 percent tax rate applicable to vehicles with output below 160 kilowatts facilitating market access for affordable EVs: 81 percent of vehicles sold in 2024 fell within this performance category. Accordingly, industrial-scale exploitation of Türkiye’s discovered REEs would precipitate intense competition with China and the United States, the preeminent players in global REE supply chains and EV production. The critical question remains whether Türkiye can navigate this arena with the same finesse it has demonstrated in prior security dossiers.

It is essential, however, not to overlook the possibility that undue emphasis on this announcement may reflect a degree of political amplification to bolster domestic standing. Experts and analyses indicate that the cited figure pertains to ore volume rather than the extractable quantity of rare-earth oxides. One assessment estimated that, from this volume, approximately 12.5 million metric tons of rare-earth oxides could be technically recoverable a substantial reserve, to be sure, yet one tempered by evident political hyperbole. Nonetheless, leveraging this discovery particularly amid Recep Tayyip Erdoğan’s final presidential term, concluding in 2028 could serve as a mechanism for sustaining the political viability of the Justice and Development Party through efficacious soft-power and economic initiatives.

From Mine to Money: A Long Way to Success

Türkiye confronts a geological endowment of exceptional promise in Beylikova: an ore deposit situated at shallow depth, thereby substantially reducing extraction costs a feature that Turkish officials consistently emphasize in their official narrative. Complementing this advantage, Türkiye already holds an unequivocal global leadership in boron, controlling more than two-thirds of the world’s known reserves. When this boron dominance is combined with the prospective rare-earth element (REE) potential, Türkiye emerges on paper as the custodian of a highly strategic portfolio of critical minerals, offering an alluring combination for both clean-energy applications and defense industries. Viewed solely through the lens of geology and subsurface resources, Anatolia is quietly evolving into a sophisticated platform for advanced raw materials in the twenty-first century—one capable of supplying both the symbolic fuel of the energy transition and the feedstock for next-generation military technologies.

The true challenge, however, commences upon shifting focus from the ore body itself to the value chain beyond extraction. Türkiye currently exhibits a conspicuous void in the midstream segments: industrial-scale refining of rare-earth oxides, complex separation processes, alloy production, and permanent-magnet manufacturing remain largely absent or underdeveloped. China continues to monopolize the entire vertically integrated sequence. To bridge this gap, Ankara would need to commit tens of billions of dollars in capital expenditure over at least a decade, directed toward mines, concentrators, refineries, separation plants, and advanced materials production lines—all within a commodity cycle as volatile as that of oil, where each new discovery can temporarily erode project margins. Should sustained long-term investment and genuine technology transfer materialize, Türkiye could, within 20–30 years, capture a meaningful percentage of global REE supply through the extraction and refining of even a fraction of the estimated 12–14 million metric tons of recoverable rare-earth oxides, thereby generating tens of billions of dollars in value-added revenue. Conversely, if the initiative remains confined to the declarative status of possessing the “world’s second-largest reserve,” this shallow, ostensibly attractive deposit risks devolving amid the deeper currents of politics and economics into yet another aborted project and a squandered strategic opportunity.

Geopolitical and Geo-economic Game: Türkiye between Russia, China, and the USA

The global market for rare-earth elements presently functions as a strategic master key to the realms of advanced technology and defense industries: possession of this key confers decisive influence over high-technology sectors, military capabilities, and, increasingly, artificial intelligence. At present, China dominates not only extraction but also refining and, to a considerable extent, the production of advanced permanent magnets. Consequently, the United States, Europe, Japan, and South Korea have for years pursued meticulous diversification of their supply chains to mitigate the risk of economic asphyxiation should Beijing withhold access to these critical materials.

In this context, the Beylikova discovery affords Türkiye the opportunity to deliver a concise yet weighty message to the West: “Invest in me, and I can assume a portion of the China risk currently borne by your systems not as a full replacement for China, but as one of several new pillars of mineral security.”

At the operational level, however, the trajectory has been markedly different. As previously noted, Türkiye lacks the requisite technology for midstream and downstream processing of the discovered minerals and remains dependent in this domain. Its initial overtures were accordingly directed toward China. Negotiations foundered, however, over technology transfer and the insistence on conducting refining operations on Turkish soil: Beijing, adhering to its established pattern, proved unwilling to relinquish proprietary processing know-how or permit the migration of value-added activities beyond its borders. Ankara, by contrast, seeks to establish factories and technological capacity domestically rather than serve merely as a raw-material conduit.

Similar impediments arose in discussions with Russia. Bilateral relations are burdened by deeper and more numerous frictions than those with China notably the Syrian dossier and Moscow has viewed with disfavor Türkiye’s emergence as the principal gas hub for the Caucasus and Central Asia, regions it traditionally regards as its exclusive sphere of influence. Following the 2022 invasion of Ukraine, Russia has exhibited even less inclination to furnish Türkiye with an additional lever of such consequential strategic valence.

Türkiye’s orientation has therefore pivoted decisively toward the United States and its Western allies, manifesting in a simultaneous geopolitical and geo-economic reorientation, accompanied by an ambition to elevate its status from mere raw-material supplier to fully fledged industrial partner. Should the Beylikova project proceed on a viable trajectory and Türkiye succeed in meeting a meaningful share of European and American REE requirements, this asset will acquire currency across multiple negotiating tables: from arms procurement and NATO standing to the Aegean disputes, Eastern Mediterranean energy developments, the Caucasus, and broader Middle Eastern engagements. Given Türkiye’s reintegration into the F-35 program, it is conceivable that Washington—motivated at minimum by the imperative of preventing a key corridor actor from drifting further into the Chinese orbit—may feel compelled to facilitate the transfer of extraction and processing technologies for rare-earth elements.

A sober assessment, however, suggests that this leverage will be taken seriously only if Türkiye can demonstrably satisfy two preconditions: first, the establishment of a robust, professional, end-to-end value chain from mining through refining; second, a degree of domestic and foreign-policy stability sufficient to ensure that supply streams are not held hostage to internal crises or regional escalations. Should these criteria be met in practice, Beylikova will transcend the status of a mere deposit; it will constitute a quiet yet enduring foundation for Türkiye’s industrial and diplomatic power in the decades ahead.

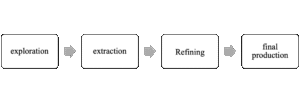

Which Part of the Rare Earth Elements Supply Chain Has a Spot for Türkiye?

If we see the rare earth element chain very compactly, we have four main rings, which are as follows:

Türkiye possesses adequate technological and operational capacity in the initial two segments of the rare-earth value chain: a substantial resource base at Beylikova, placed under the stewardship of the state-owned Eti Maden, combined with extensive experience in boron mining, provides Ankara with a solid geological and extractive foundation. Difficulties arise, however, immediately beyond the point of ore extraction. In the domains of refining and separation, Türkiye still lacks a significant industrial presence; any existing pilot or semi-industrial facilities do not yet position the country as a major global actor. At the furthest downstream end, despite notable advances in defense, aerospace, and automotive sectors, Türkiye has yet to establish a complete value chain for finished products incorporating rare-earth elements. In summary, it exhibits strength in upstream activities but pronounced weakness in midstream and downstream segments.

It is precisely this structural gap that transforms what might otherwise remain a prosaic geological report into a compelling geo-economic contest. Türkiye is deliberately seeking to transcend the traditional role of raw-material exporter and reposition itself as a regional node in the global rare-earth supply chain one that conducts both extraction and refining on its own territory and subsequently exports intermediate products and even selected end-use components to Europe, the Middle East, and Central Asia, rather than merely enriched ore. Successful execution of this strategy would effectively create a mineral-industrial corridor extending from Anatolia to European markets, analogous to the role Australia plays for East Asia in iron ore and critical minerals, yet situated at the heart of Eurasia and centered on strategically vital materials.

A realist assessment identifies two decisive factors for the project’s success: first, Türkiye’s ability to attract the requisite capital and refining/magnet-production technology without reverting to the trap of raw-material dependency; second, the maintenance of sufficient political and diplomatic stability to convince Europe and other customers that the emerging corridor is acceptably risky yet reliably resilient, rather than a conduit vulnerable to abrupt closure amid any domestic or regional crisis.

Türkiye has explicitly incorporated into its strategic calculus the contingency that a Russia–West settlement over Ukraine would enable Moscow to reassert dominance over its traditional near abroad in the Caucasus and Central Asia. To hedge against this scenario, Ankara recognizes the imperative of cultivating multiple instruments of mutual economic interdependence, thereby ensuring that its influence in these regions is buttressed by interlocking commercial ties that no single geopolitical reversal can easily unravel.

Türkiye is facing three scenarios:

1.Emergence as a Regional and Subsequently Global Node in the Rare-Earth Supply Chain

In this optimistic scenario, Türkiye realizes the vision it currently promotes primarily through media channels: transformation into a genuine regional and eventually global node in the rare-earth value chain. This would entail not only extracting ore from Beylikova but also attracting substantial investment and technology from the United States and Europe while scrupulously avoiding the raw-material-export trap. Ankara would establish at least one or two full-scale refining facilities and downstream plants capable of producing finished or near-finished products incorporating rare-earth elements, thereby creating an integrated domestic production chain. Under these conditions, Türkiye would ascend from mere reserve holder to strategic supplier, capturing a meaningful percentage of global refined rare-earth output. Its political weight within NATO and its bargaining power vis-à-vis the European Union would increase correspondingly. On the emerging world map of rare-earth actors, Türkiye would join China, the United States, and Australia at a tier comparable to Brazil or Vietnam, establishing itself as one of the top five significant players.

2.A Major Deposit but Only a Mid-Tier Role

Here, Türkiye’s most ambitious objectives remain unfulfilled, and it fails to advance into the upper echelons of the global rare-earth supply chain. A large proportion of output is exported as raw or semi-processed concentrate; advanced refining and the lion’s share of value addition either take place in China or other countries or occur within joint ventures in which critical technology and decision-making authority remain firmly in foreign hands. The outcome is a blend of respectable foreign-exchange earnings, acceptable local employment, and modest geopolitical uplift. Ankara would indeed figure as an important actor in critical minerals, yet in practice, it would remain confined to the primary supplier tier. The most lucrative segments of the value chain high technology, branding, and elevated profit margins would continue to be generated beyond Türkiye’s borders. Politically marketable and economically tolerable, this scenario nonetheless represents, from a geo-economic perspective, only partial exploitation of a historic opportunity.

3.A Project that Stalls Halfway

Environmental pressures, shifting political priorities, financial crises, or regional tensions cause the initiative to proceed at a crawl, face suspension, or experience outright rollback. Mining may continue on a limited scale, but serious refining capacity never materializes, nor does a downstream technological chain. The vast Beylikova deposit thus largely retains the status of a diplomatic bargaining chip: a resource Ankara periodically references in negotiations, yet one that exerts no decisive influence on the national budget or trade balance. Türkiye’s economic growth and geopolitical influence would then derive primarily from other vectors energy transit, defense industries, and traditional geographic advantage while the rare-earth deposit is relegated to little more than strategic background imagery in analytical presentations. Analytically, this scenario becomes more probable if Türkiye attempts to keep multiple strategic doors ajar simultaneously yet fails to commit deep, sustained investment to any single one.

Photograph: Anadolu Agency